Table of Content

When you consider the appropriate deductible level for health insurance coverage, remember that deductibles may be on each member of the family. Homeowners must meet their policy deductibles before their home insurance coverage kicks in to pay for repairs. A $1,000 deductible is better than a $500 deductible if you can afford the increased out-of-pocket cost in the event of an accident, because a higher deductible means you'll pay lower premiums. Choosing an insurance deductible depends on the size of your emergency fund and how much you can afford for monthly premiums. A $1,000 deductible is the amount you pay in the event of a claim. Some insurance companies set minimum deductible amounts in their policies.

As a homeowner and steward of your financial well-being, you have to decide which is right for you. After you choose your homeowners insurance coverages, you will need to choose a policy deductible, which is what you are responsible for paying after you file a claim. That’s why it’s important to choose a deductible that you can afford to pay out of pocket, just in case you’re stuck filing a claim. Health insurance deductibles can be complicated—especially when comparing health insurance plans or figuring out how much your current one will pay for a given expense.

How To Choose Your Deductible

Our editorial team does not receive direct compensation from our advertisers. My project is in development and I have to plan my expenses so this quote would have been useful and chosen the next year during the development of the project. Ethan wasn't understanding at all and kept insisting about how he couldn't help me. Obtaining my new liability policy was much more streamlined than other carriers/agents I've used in the past. You out and make sure everything that you own is covered and protected at the best prices. Never had a problem, and if I did they can handle my phone calls.

You pay your deductible when your property damage claim is accepted and you’ve agreed to a claim settlement with your insurance company. You don’t pay your deductible like you would your phone or utility bills — rather, your insurer simply subtracts it from the claim amount. The truth is, it's common to see an annual increase in your homeowners insurance premiums, and in many cases, it's not the result of something you did. Whether you should have a high or low deductible depends on your situation.

How to choose your deductible for homeowners insurance

If you’re not sure where to get started or which homeowners insurance company can offer you the most bang for your buck, check out the Best Home Insurance Companies for 2021. Typical homeowners deductibles can range from $500 up to $2,000. As of this past April 2021, the standard homeowners’ insurance deductible is $500. Percentages are common in disaster deductibles like earthquake insurance or wind/hail insurance policies. Homeowners who live in areas at risk for natural disasters tend to pay higher deductibles if they need to file a claim. At Insure.com, we are committed to providing honest and reliable information so that you can make the best financial decisions for you and your family.

Typically, homeowners choose a $1,000 deductible , with $500 and $2,000 also being common amounts. Though those are the most standard deductible amounts selected, you can opt for even higher deductibles to save more on your premium. It's important to understand what you're responsible for paying when you enter into an insurance contract. Depending on the coverage you have, you may have both a deductible and an out-of-pocket maximum. Fortunately there are some key differences to help you tell these apart. There’s no such thing as the perfect deductible for every policy.

How do home insurance deductibles affect the cost of insurance premiums?

You won’t pay your deductible to the insurance company like a bill. Instead, it’s subtracted from the amount the insurance company pays. You pay the rest of the money to the person or company hired to fix the damage. Often, an insurance carrier will issue several checks for different types of losses. In some cases, minor damage may cost less to repair than your deductible, so the provider won’t accept a claim. For example, if a piece of jewelry is covered by a scheduled property endorsement, a deductible might not apply.

Some health insurances limit the percentage of your medical claims they’ll cover. A copayment is the portion of a medical insurance claim that you’re responsible for paying. In most cases, a doctor’s office will request the copayment at the time of your appointment. This Blog/Vlog/Website is made available by Matic Insurance Services, Inc. for educational and informational purposes only. Matic makes no representation or warranty of any kind, express or implied, concerning the accuracy, completeness, or suitability of the information contained herein. Insurance products and services described may not be offered in all states.

But this compensation does not influence the information we publish, or the reviews that you see on this site. We do not include the universe of companies or financial offers that may be available to you. For 2022, the maximum you can spend out of pocket on in-network services for any Marketplace plan is $8,700 for an individual and $17,400 for a family. I was given a phone number to someone who supposedly could and after that person transferring me 7 different times I gave up. Quite frank, it is false advertisement to say you offer a certain type of insurance on your site, to only call and be told I cant be insured.

However, your expenses when you use your insurance are often higher than that of a person with a low-deductible plan. A person with a low-deductible plan, on the other hand, will likely have a higher premium but a lower deductible. You may still be responsible for a copayment or coinsurance even after the deductible is met, but the insurance company is paying at least some amount of the charge. In the expansive and often confusing world of health insurance, a lot of terms are tossed about. These words may be confusing to a first-time health insurance buyer or anyone trying to understand how health insurance works. Comprehensive or collision insurance — each carry their own deductible.

In such cases, you can ask the insurance company to reopen your claim if repair costs exceed the settlement payment. Typically, you must make the request within a year of the calamity. Dwelling and personal property coverages usually have deductibles, but coverages such as loss of use may not require paying a deductible. Policygenius Inc. (“Policygenius”), a Delaware corporation with its principal place of business in New York, New York, is a licensed independent insurance broker. The information provided on this site has been developed by Policygenius for general informational and educational purposes.

If you're unsure what your premium is, it's simply the cost of your home insurance policy and what you pay to your insurer to keep your policy active. If you have $300,000 in dwelling coverage and opt for a 3% deductible, you’d have to fork over $9,000 per claim before your insurance company stepped in to cover the remaining damages. While it’s typically true that a higher deductible means less in premium payments, that’s a pretty penny to shell out at once. An important thing to keep in mind is that you’ll only file a claim for damages that are equal to or above your deductible. If you experience a covered event that causes, say, $2,000 worth of damage and your deductible is $2,500, your insurance company won’t cover any of it.

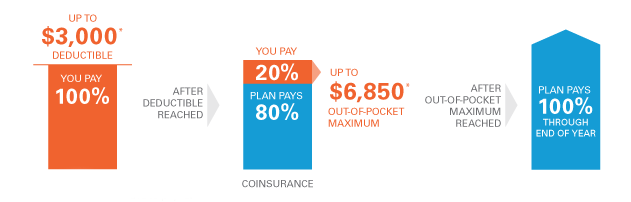

Laura Adkins has a decade of experience writing informative content and helping readers make smart decisions. She’s a former life insurance agent who also has experience in the banking industry. If, for instance, you buy a plan with a $2,500 deductible, you will pay for the first $2,500 of your medical expenses yourself. At that point, your plan will start paying some share of the expenses. If you go to the doctor, you might pay a flat $30 and the plan will pay the rest of the bill.

Deductibles for home insurance policies usually range from $500 to $5,000. Choosing the right deductibles is subjective and depends on your personal finances. When setting your deductible levels, consider two primary factors.

No comments:

Post a Comment